With everything that's gone on in DeFi in the past few months I thought I'd take the time to get back to some of my original styled content where I break down how protocols work in ways easy to understand for the everyday person but with the depth of a DeFi professional. The first and most requested one on my list is OlympusDAO and understanding the inner workings of it all.

Introduction

OHM is attempting to become a stable, non-pegged currency at its core. An ambitious goal attempted by many but still to be succeeded by any. In Olympus' view there should be a few key properties of any new currency:

A diversified treasury with valuable assets (stables, ETH, BTC and other top projects),

Ownership of its liquidity pool to collect trading fees and ensure a deep pool

Usable in other protocols, and

Optimistic outlook on the project's prospects by holders

For any viable reserve currency, you hope it’s got something backing it. Luckily Olympus does but it has a twist. Unlike other attempts in the past, Olympus employs a thing called "Protocol Owned Liquidity." We'll learn all about Protocol Owned Liquidity but let's first understand how the inner workings of OlympusDAO truly work.

Primer on Bonding

The first concept in the Olympus system is to understand how bonding works. Below is a picture I drew so that you can have a visual representation to aid you:

A user “bonds” 1 LP share consisting of DAI & OHM. There’s no official term but I like to call this liquidity bonding. You can also have naked bonding where you bond DAI directly (rather than an LP share).

Olympus then issues you “bonds” which give you OHM after a 5 day vesting period. The DAO makes revenue when it goes through this bonding process since it’s selling currency it minted to you for real financial value. This is what ensures each OHM is always backed.

90% of the revenue/profit made from the sale goes to stakers (which we’ll get to in a bit)

10% of the profit made from the sale goes to the treasury

The user receives their OHM in 5 days of which they would be profitable assuming the price of OHM has not dipped below the price they purchased (which was at a discount)

Bond Pricing

Sounds good Kerman, but how exactly is this magical discount calculated and how does it work? Great question, I had to search tirelessly to find this answer but luckily I got there in the end. In essence, we have the following dynamic when you “bond” whatever token you give Olympus. It’s a linear transfer of some USD value to Olympus and a linear transfer of OHM from Olympus to you. The time taken for this to occur is 5 days.

Before we get into the formula of how a bond is priced let’s touch on this concept of what’s known as a “debt ratio”. Basically, the number of bonds that are being issued in the process above divided by the total ohm supply is the debt ratio. This means that:

The more bonds being issued, the higher the debt ratio

The fewer bonds being issued, the lower the debt ratio

Alright, so now we have the formula for the bond price which is defined by this formula:

Now here’s where it gets interesting. If the number of bonds being issued is high, then the bond price will be higher which means that the discount to the market will be less. The fewer the bonds being issued the greater the discount. This creates a subtle mechanic where when the FOMO dies down, there’s a greater incentive to purchase bonds as a buyer. I’m not a super giga brain here but my intuition is that it smoothens out the bonds being issued over a longer time horizon.

Staking and Risk-Free Value

Alright, great job for keeping up till here. The next part which we’re going to explore is how staking works. This is where you see all the memes and high APYs.

Okay so remember how earlier we said that anyone who bonds is effectively buying OHM from the DAO? Well, now 90% of the profit goes into a pool which stakers can participate in. Doesn’t that mean that stakers can earn back the money they used to acquire the OHM via bonding? That’s where the term “Risk Free Value” comes in. It’s a term used for how much money Olympus has made from selling bonds. The risk-free value is calculated by dividing the total OHM supply by the value of the assets backing it. At the time of this article (28th October 2021) there is over $141m of risk-free value in the treasury. This in turn provides 317 days of runway for stakers to receive an 8000%+ APY (assuming no new stakers come along)

If you want to really simplify it down, the profits from the sale of bonds are distributed to stakers and can continue to do so as long as there is sufficient risk-free value in the treasury. There’s little chance of complete collapse since at the end of the day all OHM is entirely backed by real value.

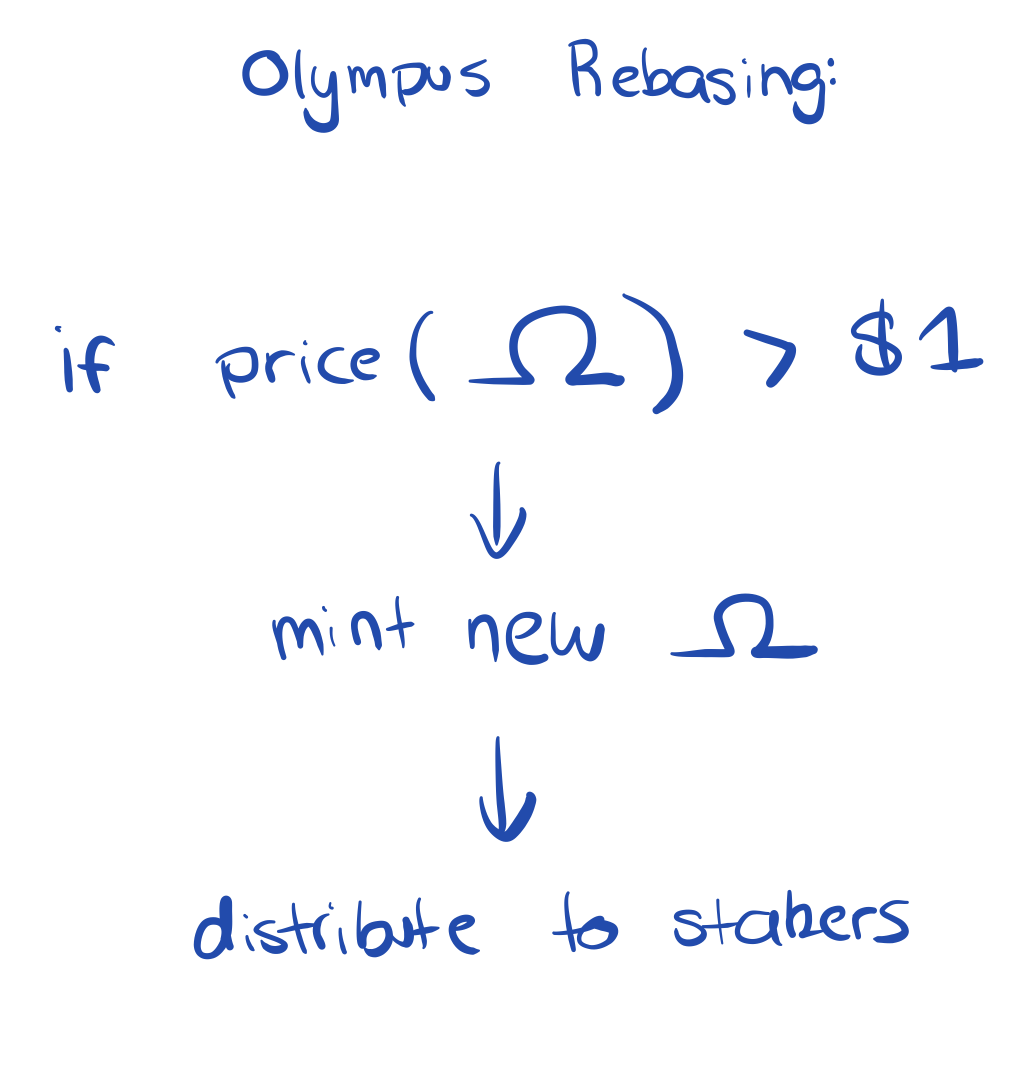

Rebasing

This is the final concept to wrap your head around but is something still worth mentioning given it demonstrates a crucial lever in the Olympus system. I drew a super simple explanation of how it works.

If there is extra OHM minted during a rebase, then there should always be sufficient Risk-Free Value backing the treasury to unwind the entire system.

Closing

There’s still plenty more I could write about Olympus including OlympusPro, Olympus 2.0, their move into more NFT things, their die-hard community but I’ll probably need to leave it for another time since this article is already getting pretty long.

Overall Olympus is a bold new attempt to redefine what it means to be a reserve currency for DeFi and does this through novel new mechanics to keep users coming back for more. While there is certainly a lot of excitement around how it works, I’m also curious to learn how it does in different market conditions. Will the high APYs sustain and if they don’t are there other sources of demand that Olympus can rely on to grow OHM? Only time will tell but there’s plenty of evidence to suggest it might.